1. Key points

- 2014 saw total domestic and cross border mergers and acquisitions involving UK companies fall to the lowest numbers recorded since 1987, when ONS first published overall total Mergers and acquisitions (M&A) figures.

- In both Q3 and Q4 2014 total domestic and cross border mergers and acquisitions continued to report lower levels of activity than seen before the 2008-09 economic downturn.

- In 2014 20 completed acquisitions of UK companies made by foreign companies (inward M&A) were reported. This is the lowest quarterly figure reported since Q1 2013 when 19 acquisitions were recorded.

- During 2014 there were 105 acquisitions of foreign companies made by UK companies (outward M&A) compared with 58 recorded in 2013, a year-on-year increase of 81%.

2. Your views matter

We are constantly aiming to improve this release and its associated commentary. We would welcome any feedback you might have and would be particularly interested in knowing how you make use of these data to inform our work. Please contact us via email: m&a@ons.gov.uk or telephone Michael Hardie on +44 (0)1633 455923.

Back to table of contents3. Summary

Mergers and Acquisitions (M&A) transactions which result in a change of ultimate control of the target company and have a value of £1 million or more are included in this release. Information on the number and value of transactions are reported, in addition to whether transactions are acquisitions or disposals.

Figures relating to mergers are included within acquisitions and those relating to demergers are contained within disposals These statistics are presented on a ‘current price basis’, which are prices as they were at the time of measurement and are therefore not adjusted for inflation.

During Q4 2014 the total number of domestic and cross border M&A involving UK companies remained relatively flat when compared with Q3 2014 and with the same quarter of the previous year (Q4 2013). There were a total of 89 completed domestic and cross-border M&A involving UK companies in Q4 2014. This total includes 40 domestic acquisitions, 26 outward acquisitions, 20 inward acquisitions and three inward disposals. This represents a decrease of 9% on the previous quarter (98) and also a year-on-year decrease of 16% on the number of domestic M&A recorded in Q4 2013 (106).

Overall 2014 saw total mergers and acquisitions activity involving UK companies fall to lower levels than experienced during the depth of the 2008-09 economic downturn and are the lowest on record since 1987, when ONS first published overall M&A data. There were a total of 376 domestic and cross border acquisitions which completed during 2014 compared with 437 in 2013, a reduction of 61 acquisitions. This represents a 14% year-on-year decrease overall of total M&A activity.

Between 2009 and 2014 the overall total average number of domestic and cross border M&A was recorded as 585 acquisitions. This total comprised of 277 domestic acquisitions indicating that this was the highest average level of M&A during the six year period, compared with inward acquisitions (160) and outward acquisitions (148). During 2009 the average number of domestic and cross border M&A recorded 172 completed acquisitions before then increasing to 299 in 2011. Thereafter the average level of overall total M&A gradually declined year-on-year falling to 125 acquisitions in 2014, the lowest annual average figure recorded since 1987.

The quarterly numbers and value of M&A activity are prone to large quarter-on-quarter movements as these data relate to specific ‘one time’ only transactions, for example one quarter can be heavily impacted by one large transaction. Therefore it can be more appropriate to analyse trends over time. Overall, during the fourth quarter of 2014 the total number of domestic and cross-border mergers and acquisitions involving UK companies remain at much lower levels of activity than before and immediately after the 2008-09 the economic downturn.

Figure 1: Number of acquisitions involving UK companies 1987 - 2014

Source: Office for National Statistics

Download this chart Figure 1: Number of acquisitions involving UK companies 1987 - 2014

Image .csv .xlsRecent M&A statistics can be put into context by comparing the low levels of recorded M&A activity involving UK companies during Q4 2014 and for 2014 as a whole, over consecutive five-year intervals since 1997 (Table 1 below).

At Q4 2014 the average number of acquisitions abroad made by UK companies (26) remained broadly comparable to the quarterly numbers recorded since 2012 (24).

The number of completed domestic acquisitions between UK companies reported in Q4 2014 (40) showed a fall of 29% when compared with the average of 56 acquisitions recorded during 2012- 2014 Q4.

Similarly to domestic M&A, the average number of acquisitions of UK companies by foreign companies during 2012 - 2014 Q4 (33) saw a fall of inward M&A activity when compared with the number of completed acquisitions recorded in Q4 2014 (20), a decrease of 39%.

The average value of inward M&A per transaction has also fallen during Q4 2014 (£133,000) when compared with the average values reported since 2012 (£159,000) a decrease of 16%. This is in contrast to the average estimated values seen for domestic (£40,000) and outward M&A (£438,000) at Q4 2014, which when compared with 2012-2014 Q4 previous average values of £28,000 and £162,000, show increases due to the inclusion of some high valued acquisitions that completed in the final quarter of 2014.

Table 1: The average number and value of M&A involving UK companies, grouped into five year intervals

| Abroad by UK companies | Overseas companies in the UK | Between UK companies | ||||||||

| Number | Value (£ million) | Average value per transaction (£ million) | Number | Value (£ million) | Average value per transaction (£ million) | Number | Value (£ million) | Average value per transaction (£ million) | ||

| 1997-2014 Q4 | 80 | 10,435 | 130 | 49 | 9,462 | 193 | 126 | 6,425 | 51 | |

| 1997-2001 | 128 | 20,402 | 159 | 54 | 9,900 | 183 | 136 | 10,921 | 80 | |

| 2002-2006 | 79 | 6,812 | 86 | 46 | 9,203 | 200 | 164 | 6,448 | 39 | |

| 2007-2011 | 67 | 8,014 | 119 | 54 | 11,813 | 219 | 121 | 4,807 | 40 | |

| 2012-2014 Q4 | 24 | 3,894 | 162 | 33 | 5,244 | 159 | 56 | 1,591 | 28 | |

| Q4 2014 | 26 | 11,393 | 438 | 20 | 2,658 | 133 | 40 | 1,617 | 40 | |

| Source: Office for National Statistics | ||||||||||

Download this table Table 1: The average number and value of M&A involving UK companies, grouped into five year intervals

.xls (33.8 kB)Domestic M&A transactions

There were 40 acquisitions of UK companies by other UK companies in Q4 2014 involving a change in majority ownership. This is similar to the number of completed acquisitions recorded in Q3 2014 (42) and represents a marginal decrease between both quarters of approximately 5%.

During Q4 2014 the value of domestic M&A was reported as £1.6 billion. This is the same value previously recorded at both Q1 and Q2 2014. However, the Q4 2014 value of domestic M&A (£1.6 billion) shows a considerable decrease of 49% when compared with the value reported at Q3 2014 (£3.2 billion).

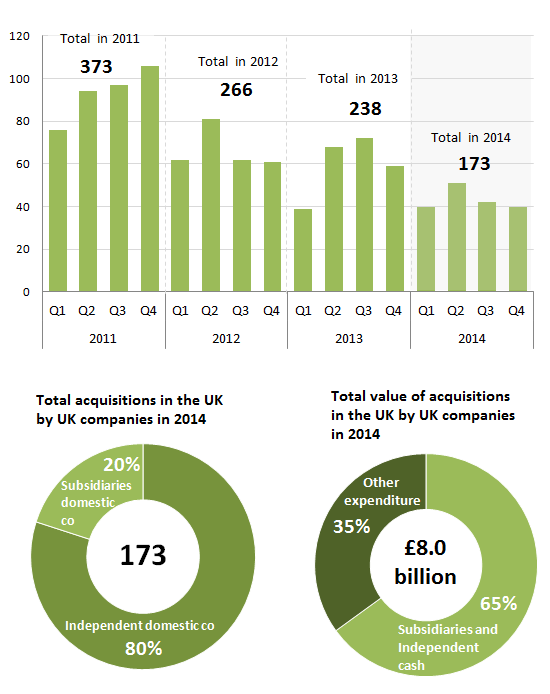

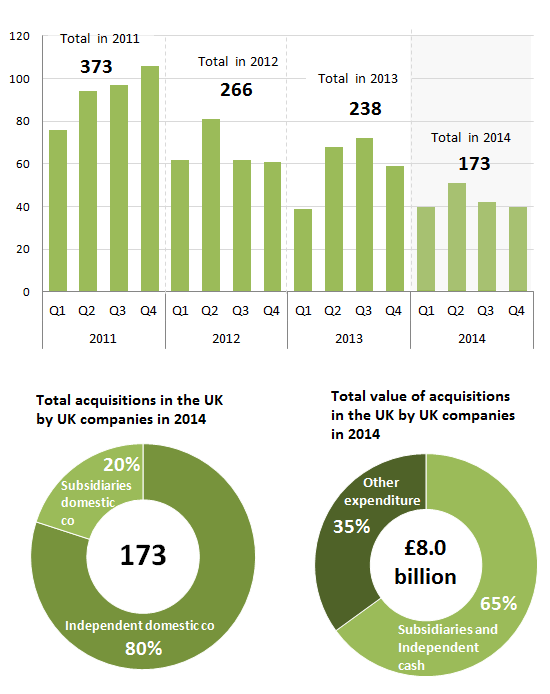

Figure 1A: Total number of acquisitions of UK companies by other UK companies 2011-2014

Source: Office for National Statistics

Download this image Figure 1A: Total number of acquisitions of UK companies by other UK companies 2011-2014

.png (42.7 kB) .xls (76.8 kB){kind=link}

Domestic M&A activity continued to decline during 2014, a decrease on the low number previously recorded in 2013 and also during the years before the 2008-09 economic downturn. This may be largely explained by the increase in the number of International Public Offerings (IPOs) reported during 2014 and to the continued restrictions in bank lending to small and medium sized businesses.

The estimates for the total number of domestic M&A continued to be dominated by acquisitions of independently controlled companies. The acquisition of an independent company means the purchase of a company in its entirety, whereas the acquisition of a subsidiary means the purchase of only a part of a company, between 50.1% and 100%.

Of the total 173 domestic acquisitions, 80% involved independent controlled UK companies, while 20% were for acquisitions of subsidiaries that were part of larger companies.

UK companies spent £8.0 billion when acquiring other UK companies during 2014. The vast majority of this expenditure (65%) involved cash transactions, while acquisitions involving the issue of ordinary shares accounted for the remaining 35%.

Inward M&A transactions

The number and value of acquisitions of UK companies by foreign companies (inward M&A) saw a continued decline of activity in all four quarters of 2014.

There were 20 inward acquisitions involving a change of majority share ownership in Q4 2014, similar to the number in Q3 2014. However, Q4 2014 recorded the lowest number of quarterly inward M&A activity since Q1 2013 (19) and some 33% lower than the number recorded previously at Q4 2013 (30 acquisitions).

During Q4 2014 the total value for inward acquisitions also declined, falling to approximately £2.6 billion, compared with £3.6 billion recorded in the previous quarter (Q3 2014).

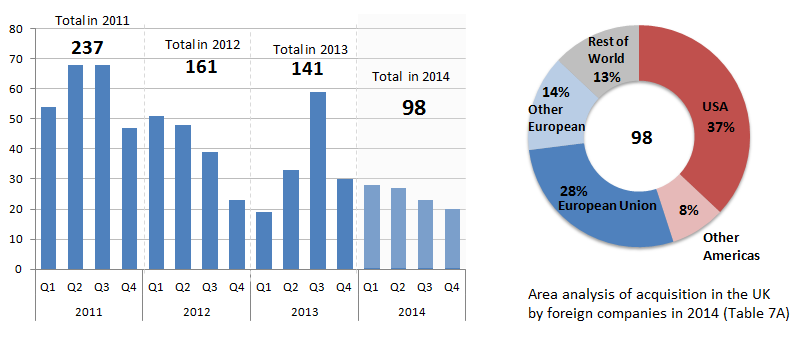

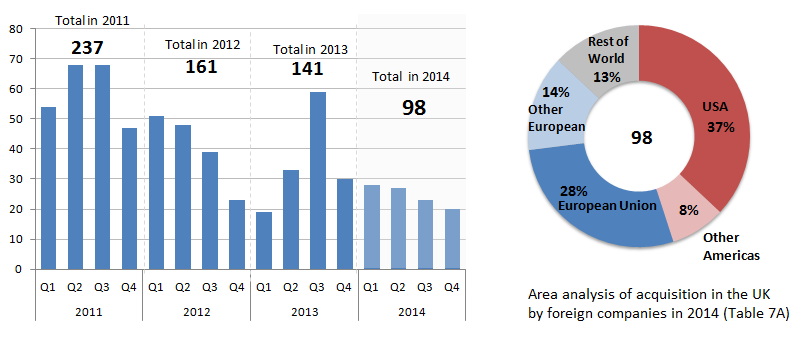

Figure 1B: Total mergers and acquisitions in the UK by foreign companies 2011- 2014

Source: Office for National Statistics

Download this image Figure 1B: Total mergers and acquisitions in the UK by foreign companies 2011- 2014

.png (34.3 kB) .xls (72.2 kB){kind=link}

For 2014 as a whole, both the number and value of inward M&A involving a change of majority share ownership have fallen to the lowest levels of activity recorded since Q1 1987 when inward M&A was first collected and published.

During 2014 there were a total of 98 acquisitions of UK companies by foreign companies, a decrease of 43 when compared with the number recorded in 2013 (141), although on a par with the number reported in 2009 (112 acquisitions) during the period of economic downturn.

The majority of the 98 inward acquisitions of UK companies which completed in 2014 were made by companies in The Americas (45%) and Europe (42%).

Outward M&A transactions

The number of completed acquisitions abroad by UK companies stayed consistent between Q2 2014 and Q4 2014, yet continued to show relatively low levels of outward M&A activity. There were 26 acquisitions abroad involving UK companies during the final quarter of 2014, broadly comparable to Q2 2014(25) and Q3 2014(24).

During the fourth quarter of 2014 UK companies spent considerably more on acquisitions of foreign companies abroad compared with previous quarters, recording a value of £11.4 billion. This considerable increase in the value of outward M&A is primarily driven by three substantive-valued acquisitions which completed during Q4 2014.

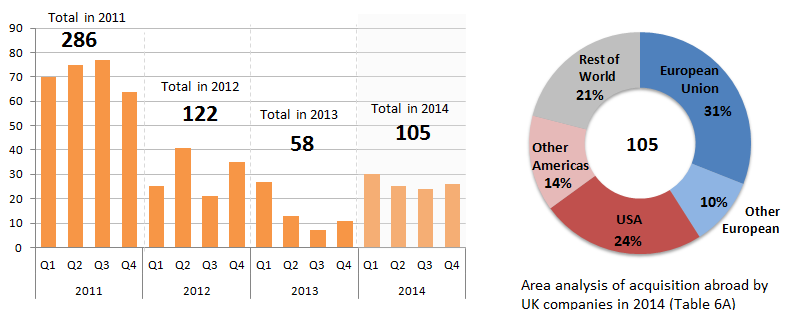

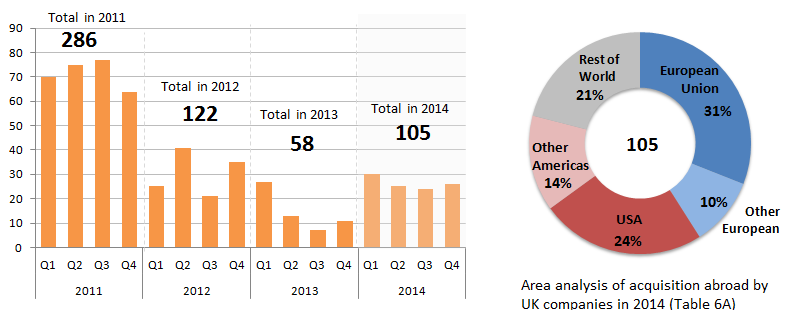

Figure 1C: Total number of mergers and acquisitions abroad by UK companies 2011- 2014

Source: Office for National Statistics

Download this image Figure 1C: Total number of mergers and acquisitions abroad by UK companies 2011- 2014

.png (34.9 kB) .xls (72.7 kB){kind=link}

Outward M&A activity experienced an upturn during 2014 for both the number and value of acquisitions involving a change of majority share ownership.

In 2014 there were a total of 105 acquisitions of foreign companies abroad made by UK companies, compared with 58 acquisitions recorded previously in 2013, a year-on-year increase of 81%. However, compared with both 2011(286) and 2012(122) the number of acquisitions have fallen.

Of the 105 outward acquisitions which completed in 2014 the most noticeable countries in which UK companies undertook M&A were in Europe (41%) and The Americas (38%).

Back to table of contents4. Transactions in the UK by other UK companies

In Q4 2014 there were 40 acquisitions of UK companies by other UK companies, involving a change in majority ownership. This is similar to the number of completed acquisitions recorded in Q3 2014 (42) and represents a marginal decrease between both quarters of approximately 5%.

Of these 40 domestic transactions there were 36 acquisitions involving UK independent companies representing the majority (90%) of total acquisitions in Q4 2014, while acquisitions of subsidiaries involving UK company groups accounted for the remaining 10%.

During Q4 2014 the total value of domestic M&A was reported as £1.6 billion, a decrease of 49% when compared with the value reported in the previous quarter of £3.2 billion.

Significant domestic acquisitions, valued at £100 million or more, that took place during Q4 2014:

Chain Bidco Plc of the UK acquired Daisy Group Plc of the UK.

Consort Medical Plc of the UK acquired Aesica Holdco Ltd of the UK.

Connect Group Plc of the UK acquired Tuffnells Parcels Express of the UK.

Figure 2: Quarterly Value and number of acquisitions of UK companies by other UK companies 2006 – 2014

Source: Office for National Statistics

Notes:

- At Q1 2010 the deal identification threshold for the mergers and acquisitions surveys was raised from £0.1million to £1.0million. There is therefore a discontinuity in the number of transactions reported as illustrated above.

- All values are at current prices (see Background Notes for definition).

Download this chart Figure 2: Quarterly Value and number of acquisitions of UK companies by other UK companies 2006 – 2014

Image .csv .xlsThroughout 2014 the estimates for the numbers and values of domestic acquisitions remained relatively stable, reporting similar levels of M&A activity at each quarter of the year.

Of the 173 acquisitions of UK companies by other UK companies during 2014, it was notable that Q2 saw the highest level of M&A activity, at 51 acquisitions. In contrast, the number of domestic acquisitions in Q1 and Q4 2014 were both recorded as 40, with a slightly higher number reported in Q3 2014 (42).

The total value of domestic acquisitions for 2014 was £8.0 billion with approximately £1.6 billion being reported in three out of the four quarters. Q3 2014 saw the highest level of domestic M&A, reporting £3.2 billion, with one large acquisition accounted for the majority of this value.

Figure 2A: Value and number of acquisitions of UK companies by other UK companies 1987 - 2014

Source: Office for National Statistics

Notes:

- At Q1 2010 the deal identification threshold for the mergers and acquisitions surveys was raised from £0.1million to £1.0million. There is therefore a discontinuity in the number of transactions reported as illustrated above.

- All values are at current prices (see Background Notes for definition).

Download this chart Figure 2A: Value and number of acquisitions of UK companies by other UK companies 1987 - 2014

Image .csv .xlsThe total value of domestic acquisitions in 2014 was £8.0 billion. This was a slight increase (4%) when compared with the value of £7.7 billion reported in 2013 and remains well below the values reported since before the 2008 economic downturn.

Overall UK domestic M&A activity has continued to decrease, a trend which was first seen in 2008 and may indicate a degree of caution still exists for UK companies before they fully commit to M&A. This may be due to companies being more specific about the M&A they undertake in order to be certain of enhancing and transforming their business for the future.

Figure 3 Summary of mergers and acquisitions in the UK by UK companies

Source: Office for National Statistics

Download this chart Figure 3 Summary of mergers and acquisitions in the UK by UK companies

Image .csv .xlsIt is possible to split out the number of domestic mergers and acquisitions into those made by independently controlled companies and those which are subsidiaries. The acquisition of an independent company means the purchase of a company in its entirety, whereas the acquisition of a subsidiary means the purchase of only a part of a company, between 50.1% and 100%.

During 2014 there were 138 acquisitions of UK independently controlled companies worth £6.1 billion, compared with 175 acquisitions valued at £4.1 billion reported in 2013. Although fewer domestic acquisitions completed during 2014, those that did were seen to be of a higher value.

The number and value of acquisitions for domestic subsidiaries also decreased in 2014 falling to 35 acquisitions worth £1.9 billion compared with 63 acquisitions worth £3.5 billion in 2013.

Figure 3A: Summary of mergers and acquisitions in the UK by UK companies, 1987-2014

Source: Office for National Statistics

Download this chart Figure 3A: Summary of mergers and acquisitions in the UK by UK companies, 1987-2014

Image .csv .xlsOther notable domestic acquisitions, valued at £100 million or more, that took place during 2014:

Quarter 1

Rentokil Initial Plc of the UK acquired Initial Facilities of the UK.

Oxford Instruments Plc of the UK acquired Andor Technology Plc of the UK.

Quarter 2

- Babcock International Group of the UK acquired Avincis Mission Critical Services Topco Ltd of the UK.

Quarter 3

Carphone Warehouse Group PLC of the UK completed the all share merger of Dixons Retail Plc of the UK.

Standard Life Investments Holdings of the UK acquired Ignis Asset Management Ltd of the UK.

Anacap Financial Partners LLP of the UK acquired Brightside Group PLC of the UK.

5. Transactions in the UK by foreign companies

Between Q3 and Q4 2014, the number of UK companies acquired by foreign companies (inward M&A) fell by approximately 13%. There were 20 completed inward acquisitions recorded in Q4 2014 compared with 23 in the previous quarter, showing a continued decline for inward M&A activity since Q3 2013 when 59 acquisitions were reported.

During Q4 2014 both the number and value of inward disposals of UK companies by foreign companies recorded lower levels of M&A compared with Q3 2014. There were nine disposals valued at £1.2 billion in Q3 2014 compared with three disposals valued at £87 million in Q4 2014. Similar to inward M&A, this low number of inward disposals recorded at Q4 2014 reflects a pattern of continued decline seen since Q4 2011 when 22 completed disposals were reported.

Figure 4: Value and number of acquisitions in the UK by foreign companies

Source: Office for National Statistics

Notes:

- At Q1 2010 the deal identification threshold for the mergers and acquisitions surveys was raised from £0.1million to £1.0million There is therefore a discontinuity in the number of transactions reported as illustrated above.

- All values are at current prices (see Background Notes for definition).

Download this chart Figure 4: Value and number of acquisitions in the UK by foreign companies

Image .csv .xlsThe value of acquisitions in the UK made by foreign companies (inward M&A) decreased by approximately 25% between Q3 and Q4 2014, from £3.6 billion to £2.7 billion. However, year-on-year comparisons show the value of inward M&A has increased by 35%, up from £2.0 billion reported in Q4 2013 to £2.7 billion in Q4 2014, the highest Q4 value recorded since Q4 2011 (£12.4 billion).

The following inward significant transactions, valued at £100 million or more, took place during Q4 2014:

Attachmate Group of the USA acquired Micro Focus International Plc of the UK.

The Cooper Companies Inc of the USA acquired Sauflon Pharmaceuticals of the UK.

Arcadis N.V. of the Netherlands acquired Hyder Consulting Plc of the UK.

Fig 4A: Value and number of acquisitions in the UK by foreign companies, 1987 -2014

Source: Office for National Statistics

Notes:

- At Q1 2010 the deal identification threshold for the mergers and acquisitions surveys was raised from £0.1million to £1.0million There is therefore a discontinuity in the number of transactions reported as illustrated above.

- All values are at current prices (see Background Notes for definition).

Download this chart Fig 4A: Value and number of acquisitions in the UK by foreign companies, 1987 -2014

Image .csv .xlsThe comparison of yearly trends for inward M&A shows that the estimate for the number of completed UK acquisitions in 2014(98) fell to similar levels to those seen during 1987 and 1988 when the numbers of acquisitions were reported as 61 and 99 respectively. From 1988 inward M&A activity increased steadily until reaching a peak in 2007 (269 acquisitions) before then seeing a gradual decline of inward activity during 2008. This has continued year on year through to 2014.

Further analysis of the trends in the value of inward M&A shows foreign companies spent £13.7 billion on acquisitions of UK companies during 2014.This represents a considerable decrease of 57% when compared with the value of £31.8 billion previously reported in 2013.

Historically the values of inward acquisitions have recorded volatile levels of activity since figures were first published in 1986. The largest value for inward acquisitions (£82 billion) was reported in 2007and thereafter a downward trend evolved with values gradually declining to the low values reported in 2012 (£17.4 billion) and 2014 (£13.7billion).

The low levels of M&A inward activity during 2014 may be due to various economic factors such as low global economic growth, continued political instability abroad and the fall in the value of the euro and other foreign currencies.

During 2014, the number and value of disposals of UK companies by foreign companies involving a change in majority ownership (20) continued to record low levels of activity similar to the numbers reported in both 2012(27) and 2013 (26).

Other inward notable transactions, valued at £100 million, which took place in the UK by foreign companies during 2014:

Quarter 1

Schneider Electric SA of France acquired Invensys Plc of the UK.

Google Inc of the USA acquired Deepmind Technologies Ltd of the UK.

BC Partners Ltd of Guernsey acquired Mergermarket Ltd of the UK.

Encore Capital Group Inc of the USA acquired Marlin Financial Group Ltd of the UK

Starwood Capital Group of the USA acquired De Vere Venues Group Ltd of the UK.

The Hain Celeastial Group Inc of the USA acquired Tilda Ltd of the UK.

Zynga Inc of the USA acquired Naturalmotion Ltd of the UK.

Markel Corporation of the USA acquired Abbey Protection Plc of the UK.

Quarter 2

The Bank of Montreal of Canada acquired F&C Asset Management Plc of the UK.

Arthur J Gallagher of USA acquired Oval Ltd of the UK.

Fairfield LP of Guernsey acquired Innovia Holdings 1 Ltd of the UK.

Graphic Packaging Holding Company Inc of the USA acquired Benson Group of the UK.

World Helicopters SARL of Luxembourg disposed of Avincis Mission Critical Top Co Ltd of the UK.

Quarter 3

Phoenix Group Holdings of The Cayman Islands disposed of Ignis Asset Management Ltd of the UK.

K+S Baltic Offshore (Cyprus) Ltd of Cyprus disposed of OCHL (Globe) Ltd of the UK.

Packaging Coordinators Inc of the USA acquired Penn Pharmaceutical Services Ltd of the UK.

Sanpower Group owner of Nanjing Xinjiekou Department Store Co Ltd of China acquired Highland Group Holdings Ltd of the UK.

Viacom Inc of the USA acquired Channel 5 Broadcasting Ltd of the UK.

Hony Capital Beijing Co Ltd of China acquired Pizza Express Ltd of the UK.

Cirrus Logic INC of the USA acquired Wolfson Microelectronics Plc of the UK.

KKR Management Holdings LP (USA) of the USA acquired OCHL (Globe) Ltd of the UK.

Hexagon AB of Sweden acquired Vero Software Ltd of the UK.

Figure 5:Area analysis of acquisitions in the UK by foreign companies

2005 to 2014

Source: Office for National Statistics

Download this chart Figure 5:Area analysis of acquisitions in the UK by foreign companies

Image .csv .xlsDuring 2014 all areas of the world recorded much lower inward M&A activity than in previous years and even lower than the dip in numbers of inward acquisitions reported at 2009, when 112 inward acquisitions were reported.

Slow global economic growth and the fall in the value of the euro, combined with lack of confidence in the stability of global M&A markets, may indicate foreign companies found it difficult to generate the internal funding required for M&A. In addition foreign companies may still remain cautiously optimistic about M&A home and abroad and thus adopt a ‘risk aversion’ approach, causing them to continue to refrain from making any substantial investment in the UK during 2014.

Back to table of contents6. Transactions abroad by UK Companies

In Q4 2014 there was an 8% increase in activity of the number of acquisitions abroad (26) made by UK companies compared with Q3 2014. The number of outward acquisitions has remained stable to the numbers reported in Q2 (25) and Q3 2014 (24). From the number of acquisitions of 30 in Q1 2014 they fell for the rest of the year and remained relatively flat.

During Q4 2014 the value of acquisitions was recorded as £11.4 billion which can be explained by three significant acquisitions (acquisitions over £100million) that completed in the quarter. In Q3 2014 the figure was £4.5 billion. Q4 2014 saw the highest value of acquisitions taking place, compared to £1.9 billion in Q1 2014. There was a noticeable increase in the value of acquisitions abroad by UK companies from Q1 2014 to Q4 2014. Q4 2011 was the last time a similar value was reported (£12.6 billion). Q2 2000 still shows the highest value of acquisitions abroad made by UK companies with a figure of £129.0 billion.

Figure 6: Value and numer of acquisitions abroad by UK companies

Source: Office for National Statistics

Notes:

- At Q1 2010 the deal identification threshold for the mergers and acquisitions surveys was raised from £0.1million to £1.0million There is therefore a discontinuity in the number of transactions reported as illustrated above.

- All values are at current prices (see Background Notes for definition).

- * Denotes disclosive figures.

Download this chart Figure 6: Value and numer of acquisitions abroad by UK companies

Image .csv .xlsThere were 105 acquisitions for the whole of 2014; not since 2012 has there been a similar number of acquisitions recorded with 122. If UK companies are not confident in the global M&A market they may not invest. As such this is a possible obstacle for companies engaging in M&A abroad. The level of M&A activities abroad by UK companies throughout 2014 (105) has decreased compared with a peak of 441 in 2007.

The following outward notable transactions, valued at £100 million or more, took place during Q4 2014:

British Sky Broadcasting Group Plc of the UK acquired Sky Deutschland AG of Germany.

British Sky Broadcasting Group Plc of the UK acquired Sky Italia SRL of Italy.

Aviva Plc of the UK disposed CxG Aviva of Spain.

The Weir Group PLC of the UK acquired Trio Engineered Products of China.

Amec Group Ltd of the UK acquired Foster Wheeler of Switzerland.

Balfour Beatty Plc of the UK disposed of Parsons Brinckerhoff Group Inc of the USA.

Tullet Prebon Plc of the UK acquired PvM Associates Ltd of Bermuda.

Old Mutual Plc of the UK disposed of Skandia companies in Germany and Austria

Figure 6A: Value and number of acquisitions abroad by UK companies 1987-2014

Source: Office for National Statistics

Notes:

- At Q1 2010 the deal identification threshold for the mergers and acquisitions surveys was raised from £0.1million to £1.0million There is therefore a discontinuity in the number of transactions reported as illustrated above.

- All values are at current prices (see Background Notes for definition.

- * Denotes disclosive figures.

Download this chart Figure 6A: Value and number of acquisitions abroad by UK companies 1987-2014

Image .csv .xlsThe total value of acquisitions made abroad by UK companies for the whole of 2014 was £20.3 billion, similar to the value of £17.9 billion reported in 2012. 2000 saw the highest recorded value on record of £181.0 billion. Since 2007 when the value of acquisitions made abroad by UK companies was £57.8 billion, the presiding years saw a decrease in the value of acquisitions to £10.1 billion in 2009. In 2010 there was a slight increase in the value of acquisitions to £12.4 billion, and subsequently a larger increase to £50.2 billion in 2011. The 2014 figure of £20.3 billion represents a 65% decrease compared to the figure recorded in 2007. Although acquisition values have increased during 2014, the number of acquisitions has declined further than the reported values in 2012. This is a reflection that the value of M&A is increasing.

The estimates of the value of the acquisitions and also the number and value of disposals abroad by UK companies during Q4 2014 and for 2014 as a whole have been suppressed in this bulletin in order to avoid the potential disclosure of companies involved in this type of M&A activity.

Other outward significant transactions, valued at £100 million, which took place in the UK by foreign companies during 2014:

Quarter 1

Smith and Nephew Plc of the UK acquired Arthrocare Corp of the USA.

Pearson Plc of the UK acquired Grupo Multi of Brazil.

IMI Plc of the UK disposed of its Beverage Dispensing & Merchandising Division of the USA.

IMI Plc of the UK disposed of its Beverage Dispensing & Merchandising Division of Germany.

IMI Plc of the UK disposed of its Beverage Dispensing & Merchandising Division of China.

British United Provident Associated Ltd of the UK disposed of Cruz Bianca Salud SA of Chile.

Pace Plc of the UK acquired Aurora Networks Inc of the USA.

Quarter 2

Rexam Plc of the UK disposed of Pharmaceutical Devices & Prescription. Retail Packing Divisions of France, Germany and the USA.

Montagu Private Equity LLP of the UK acquired Rexam Pharmaceutical Devices & Prescription Retail Packing Divisions of France, Germany and the USA.

RPC Group Plc of the UK acquired Ace Corporation Holdings Limited of China.

Savills Plc of the UK acquired Studley Inc of the USA.

QinetiQ Group Plc of the UK disposed of QinetiQ North America Inc of the USA.

Quarter 3

Vodafone Group Plc of the UK acquired Grupo Corporativo Ono S.A. of Spain.

Man Group Plc of the UK acquired Numeric Holdings LLC of the USA.

Rolls-Royce Holdings Plc of the UK acquired Rolls-Royce Power Systems (Tognum AG) of Germany.

Cobham Plc of the UK acquired Aeroflex Holding Corp of the USA.

Figure 7: Area analysis of acquisitions abroad by UK companies 2005-2014

Source: Office for National Statistics

Download this chart Figure 7: Area analysis of acquisitions abroad by UK companies 2005-2014

Image .csv .xlsBetween 2013 and 2014 outward M&A saw an increase in activity in both Europe and The Americas compared to 2013. However, this is still lower than the reported number for both continents in 2011 when Europe recorded 104 acquisitions and The Americas reported 113 acquisitions.

Additional information

Data for the following domestic and cross border acquisitions and mergers may be included in the next M&A quarterly estimates for Q1 2015.

Qatar Investment Authority of Qatar acquired Songbird Estates Plc of the UK.

Standard Life Plc of the UK sold Standard Life Financial Inc of Canada.

TPG Capital LLP of the UK acquired Prezzo Plc of the UK.

7. How our statistics compare with external evidence

The ONS estimates for domestic and cross border mergers and acquisitions, during Q4 2014 and for 2014 as a whole, appear to be in line with the views of some external commentators.

Global merger, acquisitions and disposals activity is often driven by the availability of credit and company profits as well as a sense of confidence in the economic outlook. The majority of large M&A transactions involve some element of borrowing or leveraging. Therefore when credit conditions deteriorate, as happened in the 2008-09 economic downturn, M&A activity declines. On the other hand, the process of completing an M&A transaction takes time and often there may be a lag between improving economic conditions and any quarter-on-quarter increase in M&A activity.

During 2014 the downward trend of domestic M&A may be a result of UK political instability as UK businesses experienced uncertainties about the outcome of the Scottish referendum, held in September 2014, and the impending General Election due in May 2015.

The record decline of inward M&A activity during 2014 may be in part due to the continued fluctuation and low levels of foreign exchange rates. Low foreign exchange rates may act as a deterrent and therefore possibly constrain European companies from raising the equity capital needed to pursue M&A investment in the UK.

In comparison, the increase of outward M&A activity during 2014 may be partially due to favourable foreign exchange rates which may have allowed UK companies to acquire foreign companies more cheaply. UK economic conditions have remained relatively stable throughout 2014 and this may have allowed companies to regain confidence in the M&A markets enabling them to pursue outward M&A that had previously been ’put on hold’.

The Bank of England Credit Conditions Survey - Q4 2014 reported a slight improvement in credit conditions for UK businesses in Q4. According to respondents, the spread charged on loans for large and medium-sized businesses were reported to have fallen. Despite improvements in credit conditions, net lending to businesses fell in Q4. This was mainly due to an increase in the use of non-bank sources of funding instead. For example, net equity issuance was at its highest level since 2010. However, improvement in credit conditions for small and medium-sized enterprises (SMEs) was less marked than for larger businesses in 2014. Reasons cited for this included lower access to bond and equity markets for SMEs and an improvement in profitability reducing the need for external funding or credit.

The Bank of England’s (BOE) December 2014 Agents Summary of Business Conditions explained that corporate credit conditions had improved with Banks’ interest in lending to smaller firms appeared to be increasing, suggesting some increase in lenders’ risk appetites. In sectors where access to finance had been very difficult, such as hospitality, there were some reports of companies once again being able to access bank credit.

The Office for Budget Responsibility’s Economic and fiscal outlook December 2014 stated that credit conditions and the financial system continue to normalise gradually. However, the concerns about global growth prospects have contributed to falls in commodity process and European equity prices in recent months.

Allen & Overy, an international legal practice, reported in its M&A index Q4 2014, that there has been little call for optimism since the financial crisis struck with the M&A market taking longer to recover its health than anyone expected. The report explained that the economic environment is perhaps not as settled at the end of 2014 as it was at the beginning of 2014, and that has been reflected in growing stock market volatility in recent weeks. There also appears to be growing worries about higher interest rates which could hurt investor and consumer confidence.

The OECD 2014 Investment Insights paper dated November 2014 also appears to support the downward trend of global and domestic M&A. Using data on M&A investment it stated that international and domestic M&A are both on track (based on data through Q3) to reach their lowest levels in a decade. Economic conditions that are holding back international investment in Europe would seem to be discouraging domestic investment as well.

Back to table of contents